Active vs Passive Management: The Battle of the Funds

Active vs passive management, the battle of the funds. For a long time actively managed funds were the only real options to investing in a diversified portfolio. Sure you could purchase and select your own shares but this had high brokerage costs if you were investing smaller amounts of money and you weren’t able to obtain immediate diversification.

Luckily the game has changed in this respect and there’s plenty of passively managed investments available through micro investing platforms. In this article we’re going to talk about the advantages and disadvantages of each, but first let’s define active and passive management.

Active management is where there are investment managers who make investment decisions in an effort to outperform the benchmark they are tracking. For example, an Australian equity active investment would be aiming to outperform the S&P/ASX200 index AFTER fees.

Passive managers replicate an index to gain exposure to a market or segment of a market. Because they don’t have teams of investment managers researching which companies and how much of each to hold, they’re able to charge much lower fees. Significantly lower in fact.

Sometimes the saying you get what you pay for works and in other instances it doesn’t hold true. The question is, do active managers actually outperform the market over the medium to long term?

Luckily for us Standard and Poors one of the ratings agencies, has done extensive research over 20 years on just this. The SPIVA report – Standard and Poors Indices vs Active report compares the performance of active equity and fixed income mutual funds against their benchmarks over different time horizons for markets around the world.

If we use the Australian large cap share market as an example, it compares the performance of the S&P/ASX200 against the returns of the actively managed funds.

Betashares, Ishares, Fidelity, Magellan and Schroder are all examples of companies who have actively managed funds whose goals are to outperform a specific benchmark for the asset class they are investing in.

The SPIVA scorecard shows the proportion of actively managed funds that underperformed their benchmark over a given investment horizon (1 year, 3 years, 5 years, 10 years, 15 years, 20 years). It uses net of fees returns for actively managed funds.

So let’s take a look at the results of the active vs passive management debate! The passively managed funds, exchange traded funds (ETFs) replicating the index such as STW (Statestreets ETF) and IOZ (Blackrocks ETF) outperformed 84% of Australian equity funds over a 15 year period to the end of Dec 2022. Let me say that another way, only 16% of actively managed Australian equity funds outperformed the index over a 15 year period.

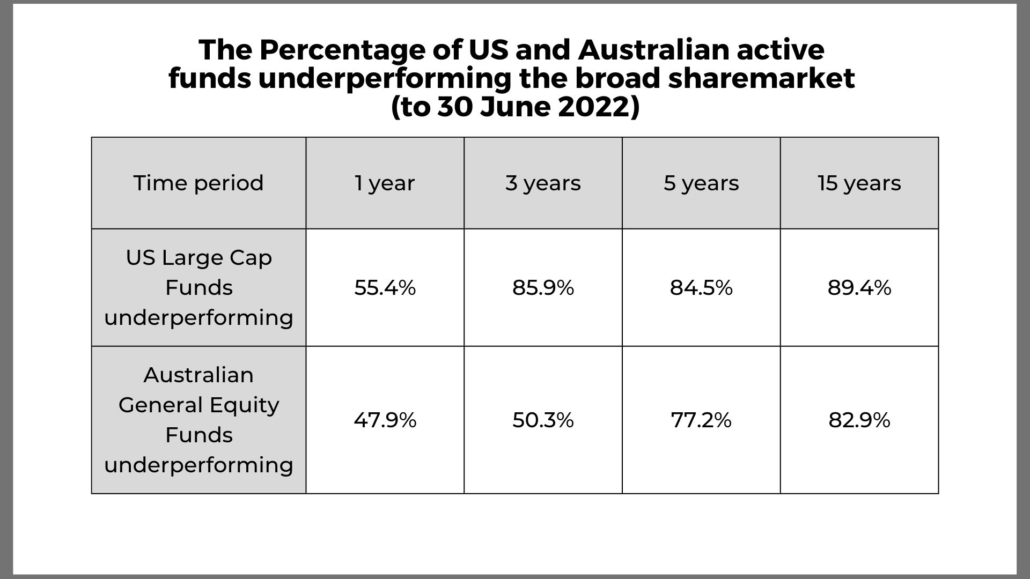

The Percentage of US and Australian active funds underperforming the broad sharemarket (to 30 June 2022)

Let’s look at the results over different time periods. Over 1 year to 30 June 2022, 47.9% of Australia General Equity funds (so actively managed funds) underperformed the index for Australian equities.

Over 3 years this increased to 50.3%, over 5 years to 77.2% and over 15 years to 82.9%.

The underperformance over 3 years, 5 years and 15 years was even larger for US large cap shares.

Every single fund has a disclaimer that says “Past performance is no guarantee of future performance” why is it then, that past performance is usually one of the first things investors look at?

Well, it’s human nature for us to be biased towards funds that have performed well in the past. But also, recency bias explains it. Recency bias is the tendency to overemphasise the importance of recent experiences or the latest information we possess when estimating future events. It’s the tendency of people to give more importance or weight to events, information, or experiences that have happened recently compared to those that occurred in the past.

So, we as humans have not only a recency bias but we’re also biased towards funds that performed well in the past…..yet the research is showing that first of all, over the medium and long term the majority of these actively managed funds don’t perform as well as the index and secondly, the funds that do outperform the market in any given year are unlikely to do it again the following year.

“Our very first SPIVA Scorecard reported that most active managers had underperformed a benchmark appropriate to their investment style over a full market cycle. Our most recent SPIVA update reports more or less the same thing.”

According to Craig Lazzara, from S&P Dow Jones Indices